Are high industrial electricity prices the most important issue in UK energy policy?

Guy Newey wrote a couple of blogs earlier this year (here, and here) which I found typically clear, thoughtful and persuasive1. But I didn't agree with all of them; and they made me think enough to want to write something myself - mostly, as I say in the about page of this blog, to get my own thoughts clear.

Guy's first post started by presenting two charts, the first of UK industrial electricity prices, and the second of UK domestic electricity prices, with the statement that these were two of the three most important charts in UK energy policy right now (the other 'most important chart in UK energy policy' shows the increase in balancing actions taken by the system operator between 2008 and 2019).

Guy says the price charts are important for two reasons:

-

Economics: high electricity prices damage competitiveness, in particular in manufacturing and industry; and

-

Politics: high electricity prices support the argument that 'Net Zero is damaging growth, so we should stop.'

Before I go on, a caveat: politics, geopolitics, and the energy system have changed a lot since Guy wrote his piece and I strated thinking about it. I don't think I have a very clear view here, and I totally reserve the right to change my mind about this in future.

The Economic / Strategic Claim

Guy's first piece is really about the second claim - about the politics of high electricity prices.

But it was the first claim - the economic / strategic claim - that made me stop and think. I found myself asking: are high UK industrial electricity prices, relative to other countries, the most important thing in UK energy policy right now from an economic and strategic perspective?

My short answer is, basically, what Tom Forth said in this blog post: "Not good, but fine." - how important to UK growth is getting industrial electricity prices down?

An alternative view is set out in this post by Jonno Evans: "The Energy Theory of Everything"

And Richard Jones also covers a lot of what I'm going to say here: "The decline of UK industry wasn’t caused by high energy prices, but they’re a big problem now, for what’s left of it"

My slightly longer answer involves deconstructing the argument and looking at the data.

I think the claim that high industrial electricity prices, relative to other countries, is one of the two or three most important things in UK energy policy right now, would only be true if:

-

Electricity costs are a large part of the cost base for a wide range of UK economic sectors2; or

-

Electricity costs are a key factor driving or impeding future economic growth in key sectors of the UK economy; or

-

Electricity costs are a large part of the cost base of otherwise 'strategically important' sectors.

So, are these three things true?

I think the answer is, at best, 'maybe'.

Premise 1: Are electricity costs a large part of the cost base for a wide range of the UK economy?

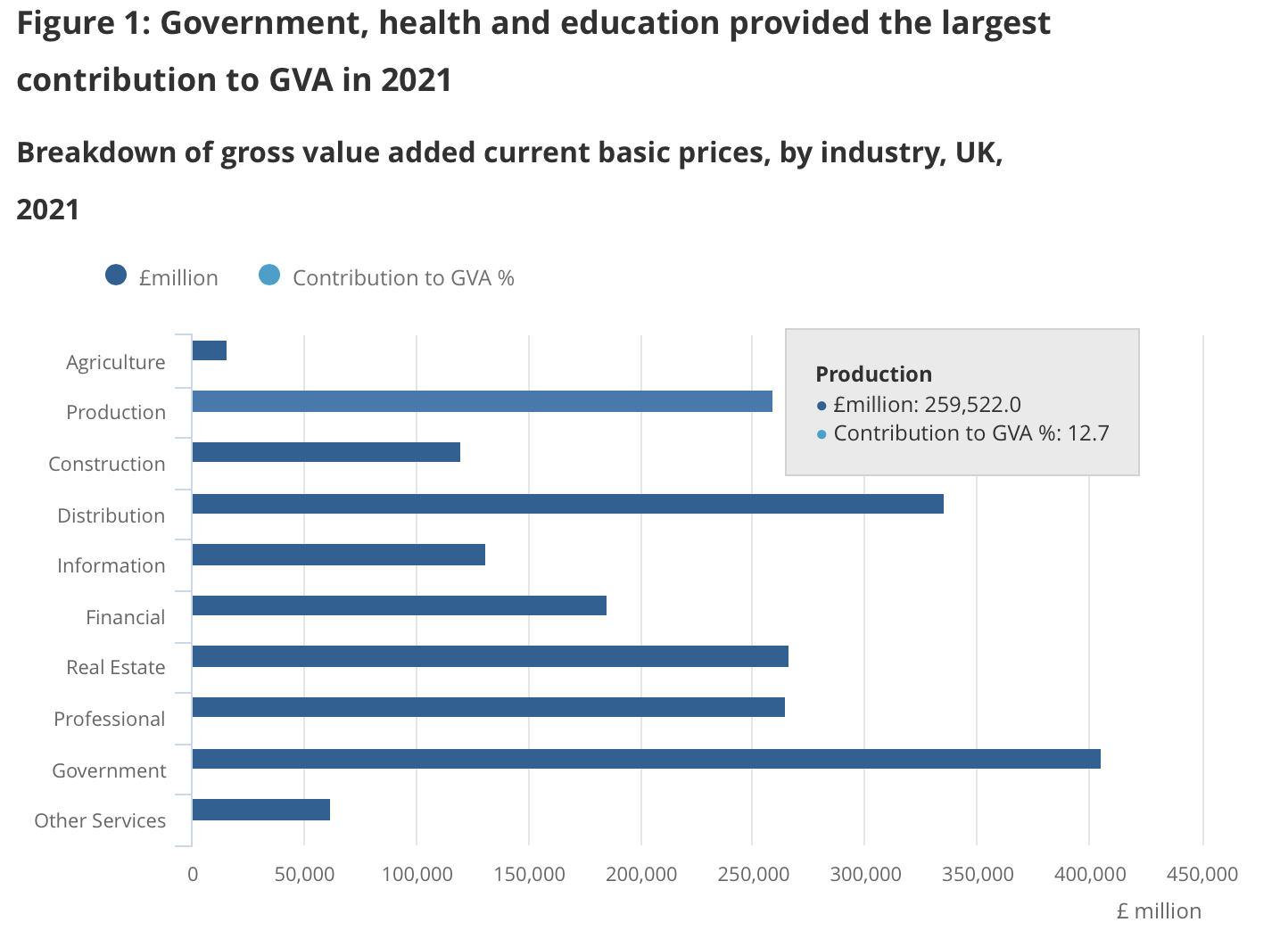

Here is a chart from the ONS3 that breaks down the contribution to UK GVA by macro sector:

"Production" (which I understand to mean all manufacturing, industry, food and drink processing, etc.) contributes 12.7% of UK GVA.

Information, Financial, Real Estate, Professional, and Other Services together contribute 44.4% of UK GVA. Government contributes 19.8%. Construction contributes a further 5.9%. In total, these sectors contribute 70.1% of UK GVA.

I don't believe these are energy- or electricity-intensive sectors. I don't have data on how much of these sectors' cost-base is electricity costs, but I'm prepared to assert that it's not true that electricity costs are a large part of the cost base for sectors that make up over 2/3rds of the GVA in the UK economy.

I think it is true that electricity costs are a large part of the cost base of production, but production is a relatively small part of the UK economy.

As an aside, distribution contributes 16.4% of UK GVA; but this is not yet heavily impacted by UK electricity prices, as we're only just starting to move up the S-curve of electrification of distribution. Looking forwards, it seems very clear to me that we will electrify almost all light and heavy goods vehicles over the coming decades. So continued high electricity costs could slow down the pace of electrification of light and heavy goods vehicles; and would increase the relative costs for this sector as we do electrify. So I'll score this as half marks in favour of the thesis that high electricity prices are strategically important for this sector.

My conclusion in relation to the first thing that would have to be true - Electricity costs are a large part of the cost base for a wide range of UK economic sectors - is that this is not true.

Premise 2: Are electricity costs are a key factor impeding future economic growth in key sectors?

This question is much harder to answer: as the saying goes, making predictions is hard, especially about the future. And the answer is also very dependent on one's view of what sectors will be most important for the future economic growth of the UK.

I'm not an expert on industrial strategy; but since that's not stopping anyone else writing about it at the moment, I'll be unwise enough to set out my thoughts.

Firstly, as the statistics above show, the UK today is primarily a service economy. Importantly, this includes both low (economically) value-added services, and high value-added services. I think a lot of our economic growth is going to continue to come from services; and a sensible industrial strategy would recognise our strengths in this area and seek to capitalise on them. And in general, these are not electricity-intensive. So relatively high electricity prices wouldn't seem to be a barrier to growth in these sectors.

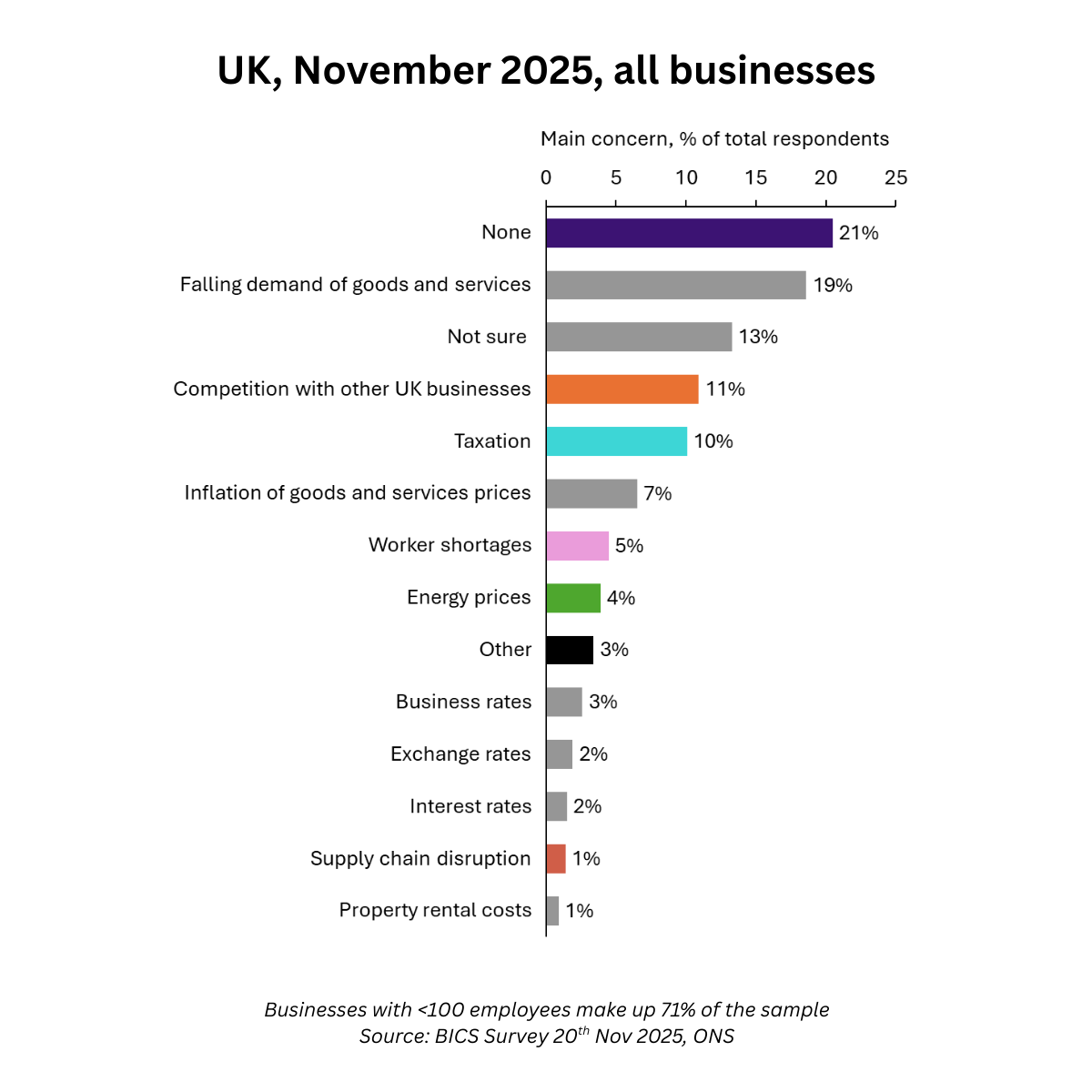

And it's worth also looking at this chart - which I came across in Lucy Shaw's substack here - indicating that energy prices are the main concern for only 4% of UK businesses:

But let's look at manufacturing and industry, which is the area where electricity costs could be an important factor in undermining the UK's competitiveness and future growth.

We can look at some good data to help understand what's going on here: DESNZ publishes international statistics on industrial electricity prices (here); and we can get data on manufacturing as a share of GDP via Our World in Data (here)4. I'm going to use data from 1990-2023, as that's the longest time series I can find in both sources.

What do these data tell us?

Firstly, as the chart below shows, UK manufacturing as a % of GDP has decreased a lot in that period - from over 16% In 1990, to just over 8% in 2023.

UK manufacturing as % GDP vs. OECD comparators, 1990-2023

Looking at the annual change, indexed to the value in 1990, we see that most of that change happened between 1990 and about 2009

UK change in manufacturing as % GDP 1990-2023, 1990 = 0

So, what was happening to UK industrial electricity prices over that period?

UK industrial electricity price (pence/kWh) vs. IEA comparators, 1990-2023

The answer seems to be, there were two distinct periods: from 1990 to around 2004, UK electricity prices were pretty stable; then from 2005 onwards, they started to increase rapidly, with a very significant acceleration from 2021 onwards due to the huge increase in gas prices resulting from the Ukraine-Russia war.

If we look at the period 1990-2023 as a whole, there is a clear medium-strength negative relationship between UK industrial electricity prices and UK manufacturing as a % of GDP:

UK industrial electricity price (pence/kWh) and manufacturing as % GDP 1990-2023

A linear regression shows:

-

R²: 0.46

-

Correlation coefficient (r): -0.68

-

Slope: -0.4

-

p-value: 0.00001 (highly significant)

The negative correlation means that higher electricity prices are associated with lower manufacturing as % of GDP: for every 1 pence/kWh increase in electricity price, manufacturing as % of GDP changes by -0.400 percentage points. An R² of 0.46 means that 46% of the variation in UK manufacturing share of GDP can be predicted by electricity prices in the period 1990-2023 (a moderately strong relationship).

We can also see that the majority of the reduction in UK manufacturing as a % of GDP after 1990 came in the period in which industrial electricity prices were relatively stable - i.e. 1990-2004 - and not in the period in which UK industrial electricity prices were rapidly increasing.

In fact, if we run a regression between the two variables just for 1990-2004, we get a positive correlation - higher electricity prices are associated with a higher manufacturing share of GDP in this period!

(NB - one could be accused of p-hacking, hence why I'm not showing charts and full results for this sub-period. But it's certainly the case that this data strongly suggests that increased industrial electricity prices, while potentially important, are far from the only reason for a reduction in manufacturing as a share of GDP in the UK).

International Comparisons

It\'s also useful to compare the UK to other 'advanced' economies. In my view, this shows us three interesting things:

Firstly, the UK has been in the top half of countries for industrial electricity prices throughout the 1990-2023 period, moving very clearly to being one of the most expensive countries for industrial electricity after 2015.

UK rank for industrial electricity prices vs. IEA comparison group 1990-2023 (higher rank represents higher UK price relative to other countries)

Secondly, looking across all countries we see a strong negative relationship between industrial electricity prices and manufacturing as a share of GDP.

Industrial electricity price (pence/kWh, left hand axis) and manufacturing as % GDP (%, right hand axis), selected IEA countries, 1990-2023

Here's where things get interesting.

I looked at the relationship between industrial electricity prices across countries, and over time, in four ways:

- Firstly a simple pooled OLS (which dumps every data point from every country into one big 'bucket' and draws a line through it). This appears to weak evidence of a link; but conclusions are likely unreliable due to Simpson's Paradox.

- Secondly a simple one-way fixed effects model. This shows a significant negative relationship between industrial electricity prices and manufacturing as share of GDP: a 1 pence/kWh increase in industrial electricity prices was associated with a nearly 0.25 percentage point decline in manufacturing’s share of GDP. This aligns with the "deindustrialization hypothesis," which suggests that rising energy costs drive industrial flight or reduced output. But the question remains - does this really show causation, or just correlation?

- A two-way fixed effects model. The significance found in the one-way model disappears on introduction of time fixed effects in the two-way model (p=0.838). This transition suggests that the results in the simpler model were largely driven by spurious correlation.

- A time-lagged two-way model. This model shows that, even when looking back two years, the price signals aren't strong enough to predict changes in the manufacturing-to-GDP ratio.

| Model | Specification | Price Coefficient | P-Value | Significance | Result Interpretation | |---|---|---|---|---|---| | 1. Pooled OLS | Baseline (No Controls) | -0.027 | 0.579 | None | No significant global correlation detected. | | 2. One-Way FE | Country Fixed Effects | -0.247 | < 0.001 | High (***) | Significant negative link; likely capturing shared global deindustrialization trends. | | 3. Two-Way FE | Country & Time Fixed Effects | +0.022 | 0.838 | None | Relationship vanishes after controlling for global year-to-year shocks. | | 4. Distributed Lag | Two-Way FE + 2-Year Lags | -0.052 (Lag 2) | 0.590 | None | No delayed response detected even after allowing 24 months for industrial adjustment. |

The two-way fixed effects model, effectively "nets out" the global background noise. This model shows that when a specific country’s electricity prices spiked relative to the global trend, that country did not see a statistically significant drop in its manufacturing share compared to its peers (and the lagged model shows this remains the case at least over a two-year period).

So - what's going on?

Well, the countries shown are all developed economies. Over the 1990–2024 period, many developed economies experienced two simultaneous but independent trends: - Structural Deindustrialization: A global shift toward service-based economies driven by automation and comparative advantage. - Energy Transition: A general upward trend in nominal electricity prices due to inflation and carbon-pricing policies.

By "netting out" these global year-to-year shocks, the model shows that idiosyncratic price spikes within a specific country do not result in immediate or outsized losses in manufacturing share relative to global peers.

If we compare the UK and Germany, for example, we see that German manufacturing represents a much higher % of GDP than in the UK - but for almost the entire 1990-2023 period, it also had slightly higher industrial electricity prices than the UK:

In my view, an important alternative explanation for the reduction in manufacturing as a % of GDP, is that in the UK we've had around 40 years of very clear industrial strategy, the objective of which was to build very strong finance, services, and (perhaps to a lesser extent) life sciences industries - which was very successful!

More importantly, the premise being explored in this section implicitly assumes that, if we could just reduce industrial electricity prices, re-industrialisation would follow. I've written a bit on this here...well, let's just say that the existence or not of deep process knowledge and highly interwoven supply chains is probably also an important factor that will determine how effectively and/or quickly the UK could re-industrialise, even if it had cheaper electricity.

Summing this section up - looking at the premise that Electricity costs are a key factor driving or impeding future economic growth in key sectors of the UK economy, I think there's pretty good statistical evidence that electricity costs are an important factor in driving or impeding growth in manufacturing in the UK. So, to the extent to which manufacturing - or particular sub-segments of manufacturing - are key actual or potential growth sectors of the UK economy, then high electricity costs matter.

They are not, however, the only factor, and not clearly the most important factor, in the growth or otherwise of these sectors.

Premise 3: Are electricity costs are a large part of the cost base of otherwise 'strategically important' sectors?

The main line of thought I hear about the impact of high electricity costs on 'strategically important' sectors recognises that the world has changed a lot in the past year. China's emergence as a manufacturing superpower has become clear to many people. There is a war in Europe. And a second Trump presidency has led to tariffs and potentially significant disruptions to global trade, including in strategically important things like computer chips, advanced magnets, batteries, refined rare earth metals themselves, and gas.

In response, companies and policy-makers in Europe, in particular, are re-thinking the extent to which they can rely on fairly free global trade to supply their needs; and are looking at their industries and asking themselves 'Which of these are so strategically important that we need to have our own domestic supply, independent from both the US and China - no matter the cost?'

Answers to that question seem to include (at least): everything military, from drones to fighter jets to ships; all of the computer hardware and software that drives them; AI; the steel to make them; energy, batteries and vehicles; and all of life sciences.

And people then say 'electricity costs are too high in the UK to be able to create competitive industries in these sectors'.

What do I think about this?

Looking at the manufacturing sectors, the data we've just looked at do show that high electricity costs are pretty strongly correlated with reduction in manufacturing as a % of GDP. And it's certainly plausible that this really is a causal relationship - i.e. high relative industrial electricity costs inhibit the growth of manufacturing - though this is far from the only factor.

Looking at AI specifically - I'm not convinced that energy costs are as important a factor as they are made out to be. I understand that the energy costs of training models and running inference once they are trained are high. But we also see the 'solution to high prices is high prices' effect - AI companies are making rapid developments in reducing the energy requirements of training and running models, through both software and hardware. Perhaps more importantly, my read is that the quality and reliability of electricity supply, and above all about whether a data centre can get a connection to the grid at all, is much more important to AI companies than [costs]{.underline} per se.

Coming back to the question at hand - which sectors are so 'strategically important' that the UK needs to have its own manufacturing capability; and which of these are highly sensitive to electricity prices?

The truth is, I don't have a clear view of what sectors are really 'strategically important' for the UK - after all, it depends what your strategy is! One of the key questions in strategy is choosing 'where to play'. And those choices are often more constrained than people like to think.

It seems to me that a lot of the discussion of the importance of manufacturing and industry has a strong sense of 'generals fighting the last war' - whether people are harking back to the trentes glorieuses period, or further back to when the UK had a comparable position to that of the US and China today (and an empire that enabled that position).

It also veers towards a very autarkic view of the future - which I'm not sure the UK is in a position to sustain (even if that were desirable).

I realise I haven't really come to a conclusion on this premise. I will conclude by noting that not everything can be a 'strategic priority'.

Overall then, what do I think?

To repeat for those at the back: yes, high relative electricity prices inhibit competitiveness, especially of electricity intensive sectors; and yes, it would be better if we had lower relative and absolute electricity prices.

But, I find it hard to conclude that high UK industrial electricity prices, relative to other countries, are the most important thing in UK energy policy right now from an economic and strategic perspective. Electricity intensive sectors are not the majority of the UK's economy. Not all electricity intensive sectors are key to future economic growth. Even in those that are, electricity costs are not the only important factor that influences the growth of those sectors. And it's not clear that electricity-intensive sectors are all strategically important in some other way.

That, of course, naturally leads to the question of what is the most important thing in UK energy policy right now from an economic and strategic perspective?

Something I'd like to think and write more about in future.

-

I'm not just saying that because Guy's my boss.

-

I actually think it's important that we consider costs in relation to revenues, not just as a proportion of the firm/sector's cost base. If a firm/sector is highly profitable, then a high proportion of its costs is still a (relatively) small number. But I don't think this is worth splitting hairs over for the purposes of this piece.

-

Office for National Statistics (ONS), released 31 October 2023, ONS website, compendium chapter, The industrial analyses, UK National Accounts, The Blue Book: 2023

-

World Bank and OECD national accounts (2025) - processed by Our World in Data. "Manufacturing, value added (% of GDP)" [dataset]. World Bank and OECD national accounts, "World Development Indicators 122" [original data]. Source: World Bank and OECD national accounts (2025) - processed by Our World In Data